Investments and expenditure are necessary for any business to achieve and maintain the capacity to deliver service. However, it is equally important to ensure that you get the most value out of each investment made or expense incurred. And indeed many entrepreneurs do very well in generating sales revenue for their budding and growing businesses, but fail short in identifying, managing and controlling their costs. This makes them loose profit margins and even post losses from reasonably good sales volume. Your ability as an entrepreneur to control your costs is very key to your business survival, profitability and growth.

Investments and expenditure are necessary for any business to achieve and maintain the capacity to deliver service. However, it is equally important to ensure that you get the most value out of each investment made or expense incurred. And indeed many entrepreneurs do very well in generating sales revenue for their budding and growing businesses, but fail short in identifying, managing and controlling their costs. This makes them loose profit margins and even post losses from reasonably good sales volume. Your ability as an entrepreneur to control your costs is very key to your business survival, profitability and growth.

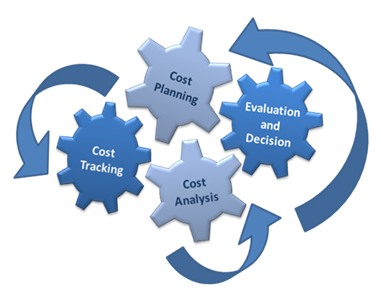

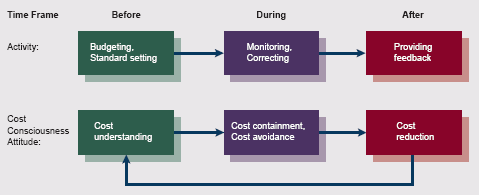

Cost control involves monitoring and regulating expenditure in your enterprise. The objective is to optimise costs even before they are incurred. This should cover investments in fixed and current assets as well as operating expenses. Cost control measures have the common objectives of improving business cost-efficiency by reducing costs, or at least restricting their rate of growth.Cost control measures help you increase productivity, competitiveness, and profitability.

No matter the size and stage of your business, you should use cost control methods to monitor, evaluate, and consequently enhance the individual efficiency of specific areas or functions as well as the whole enterprise. How can you therefore control your costs?

Understand your costs: There are different types of costs. Generally, costs are classified as either being ‘fixed’ or ‘variable’. Fixed costs are those costs that are not directly related to sales or production volumes. They typically include such costs as rent, insurance, some types of utilities, or for running the business, such as salaries, advertising etc. Fixed costs can change over a period of time. However, the change (increase or decrease) is not directly correlated to production or sales. Variable costs, on the other hand, are directly related to business activity. Raw materials and inventory are good examples of the variable costs of a business enterprise. Variable cost elements will normally increase or decrease with increase or decrease in production and sales.

Understanding which costs are fixed and which are variable in your business will help you keep an optimum cost structure that helps you maximise returns at any particular production/sales capacity range. In addition to understanding types of costs and their structure in your business, you also need to under their dynamics, that is how the costs change against other business variables such as time and production capacity.

As a thumb rule, and as much as is possible, you should always aim to keep your fixed costs to the barest minimum possible. The only caution to be exercised whilst working to achieve this objective is to ensure that you do not compromise your capability to produce and deliver your goods and services. Indeed, sometimes you have to incur additional costs in order to increase production, efficiency, sales etc. The key is to formulate your whole business strategy to achieve cost-reduction without negatively impacting your business.

Know your cost and profit centres: Units and departments within a business enterprise can be broadly classified into ‘Cost’ or ‘Profit’ Centres. A cost center is any unit of your enterprise that adds to the cost of running the company but not directly responsible for generating income. Usually, cost centres tend to be ‘support’ units that are necessary for the profit centres to operate optimally. Staff of a cost centre are responsible for its costs but do not, primarily, generate income. Sometimes obviously, cost centres may generate ‘other’ incomes for your business. Such incomes are typically very small and contribute quite minimally to the overall profit of your business. Depending on a business type, departments such as human resources, IT, and accounting are considered cost centres. Profit centres on the other hand are other identifiable departments or units of a business enterprise that significantly contribute to the overall financial results of the business by generating sales revenue and income. Depending on the size and nature of a business, profit centers are normally given responsibility to target certain percentages of the total revenue the business plans to generate over, say a year, and are given adequate authority to control their costs to achieve the set and agreed targets. Your sales department is an example of a profit centre as it generates sales revenues from which significant net income of your enterprise is made.

Understanding which units of your business are cost or profit centres will help you articulate relevant strategies for each to achieve its functional objectives at the most optimal cost levels.

Set up a system to capture your costs: Next, you should set up a system to capture and collate all costs, and of course other key financial and production information. Nowadays, even for the smallest businesses, there are very simple accounting softwares available to capture all your relevant costs and generate basic reports that will help you make decisions. Work with your accountant or consultant to set up a system that will give you all the relevant information you have identified as required. The information should be regularly and readily available for analysis and decision making. A good accounting system is primary to your cost control process.

Set up a system to capture your costs: Next, you should set up a system to capture and collate all costs, and of course other key financial and production information. Nowadays, even for the smallest businesses, there are very simple accounting softwares available to capture all your relevant costs and generate basic reports that will help you make decisions. Work with your accountant or consultant to set up a system that will give you all the relevant information you have identified as required. The information should be regularly and readily available for analysis and decision making. A good accounting system is primary to your cost control process.

Thereafter, you should plan your cost control measures and communicate them clearly within your enterprise. Staff should be sufficiently motivated to achieve cost targets without compromising service delivery.

Create a budgetary system: Planning and budgeting are very important tools in your cost control process. Create your monthly budgets that adds up to your financial year budget. The annual budget should also be broken down on unit and functional basis so that all responsible officers are clear about what is expected of them and their units. Be ambitious in your cost control effort. But ensure that you work on sound and realistic assumptions and bases. It is important you understand what is happening in your national economy; study what is happening in your industry and benchmark with the very best. This will mean you set up standards against which you can measure and assess how your are doing.

Your budget will be be then become a yardstick against which you will assess your performance. Aim to be among the best in your industry. Your budget will help you asses whether or not you are operating at, below or above projected costs. Variance must be understood so that you are clear why you are operating at the levels you are. Fiscal discipline is key to business success. Just ensure that your cost control efforts cuts out only the ‘fat’ and not the ‘muscle’ of your business.

Identify key costs and how they can be minimised and controlled: Costs can generally be classified under such headings as labour, materials, and overheads. These headings can also be sub-divided into various sub-headings. For each business, it is important that you identify specific ways to control your operating costs. Do not underestimate any savings that can be achieved. Over time, minor savings can add up to substantial amounts. Various tools such as Materials Flow Study, Work Study Analysis, Quality Control, etc all help to identify areas you can reduce your costs. Aim to identify and introduce simple and innovative techniques that can significantly reduce your costs. Discuss with key people across levels and you will surprised how your staff and customers will help you reduce your costs. You can even learn how to cut costs from your competitors by learning how they do some of the things they do.

You need to have a company-wide philosophy that realises each cost as being key, but some will definitely be more ‘material’ than others. Start by working on the ‘material’ costs. Identify exactly how you can bring down and keep each identified material (as in key) cost to the barest minimum possible level. This is where your procurement system should also work to give you maximum value for all goods and services purchased. To do that, you will need to set targets in advance (your budget would have provided this), measure actual achievements and compare it with plans to ascertain variances. Both positive and negative variances should also be reviewed to ascertain what caused them. Adopt the necessary techniques that will help you assess your cost management performance. Such techniques include, but are obviously not limited to, Budgetary Control, Standard Costing, Ratio Analysis, Variance Analysis etc. Start from the simplest approaches and keep improving. Remember that improving cost efficiency is a continuous challenge. Face it proactively before your competition forces you to. It may be too late by the time you realise that.

In another post soon to come up, we will present various specific ways you can minimise your operating costs.